Just like Neo’s ability to stop bullets

The Singapore government introduced a new round of cooling measures at around 11.45pm on 29th September 2022 with effect kicking in on 30th September 2022 Friday. It’s about time the government do something else future will sure have difficulty owning a home in Singapore.

In just one move, condo downgraders and those who wishing to purchase larger HDB units practically hit an invisible brickwall.

The new measures includes:

- For HDB loans, the loan-to-value (LTV) limit has been lowered from 85 per cent to 80 per cent.

- For property loans from private financial institutions, the medium-term interest rate floor – which is used to compute the total debt servicing ratio (TDSR) and the mortgage servicing ratio (MSR) – has been raised by 0.5 percentage point.

- For loans granted by HDB, the agency will introduce an interest rate floor of 3 per cent for computing the eligible loan amount.

- The loan-to-value (LTV) limit for HDB loans will be lowered from 85 per cent to 80 per cent.

A 15-month wait-out period for private home owners before they can purchase a non-subsidised HDB resale flat. The new rule will also apply to those who sold their private property prior to submitting an application to buy a resale flat.

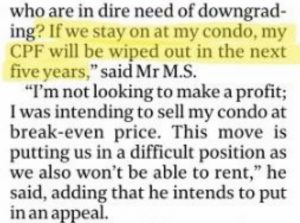

Wiping out of CPF

I am not surprised when I read such news about being asset rich but cash poor. 2022 is a damn lousy year whereby S&P had already sunk close to 25% YTD against a backdrop of relentless interest rate hikes, those that still has a huge monthly home loan to service every month, the last thing they need is another cooling measure that was announced by the government.

And the bad news will just kept coming. As Fed Chair Powell already vowed to raise rates to fight inflation ‘until the job is done’

Sometimes it is better to be contended

Having a fully paid HDB home is life’s best joy. There’s no need to worry about monthly mortgage loan, refinancing with floating or fixed rate, 1-month or 3-month SORA etc. Every night just sleep in peace.

But of course one also hopes that he or she don’t kena the stupid SERS like AMK SERS residents lar. Just imagine we already fully paid for our HDB and when we are reaching retirement age, we were ‘forced’ to take on new loans again.

I will not repeat the same frustrations in this article but you can read more here and here.

So what did I learn from this entire Sep 2022 cooling measures?

My AIA ‘Financial Adviser’ bought a EC in the recent years. He is still serving out his MOP. I supposed with the slowing down of economy, his income was affected and he was thinking of downgrading back to a HDB by selling his EC.

Well, this latest cooling measures had 100% dashed his hope of ‘downgrading’ back to a HDB.

For me, when I 1st stepped into the workforce, my 1st home must be a HDB. And even during the later stage in life when I was able to afford to upgrade my lifestyle, I would never buy a EC.

A property agent once tried to sell me the idea of buying an EC at about $500K plus and can sell for $1M after TOP. According to the agent, with the money, I can buy back the HDB and will still have cash on hand. The agent also said ‘a lot of people are doing that’.

But when I asked the agent if I can buy back this very HDB unit that I am living now with that $1M, the sense of confident suddenly gone like the wind.

HDB is always the Plan B if something goes wrong. I would rather pay more to buy a condo and still get to keep my HDB.

So what did I learn from this cooling measure? Well, the era of cheap money is over. Less debt also equals to less headaches in time of uncertainties. That was also why I will never pay that kind of obscene money for Central Weave.

I don’t want to be the frog that is being slowly cooked alive.